Sacramento Market Update | October

Past Market Updates

Past Market Updates

Quick Take:

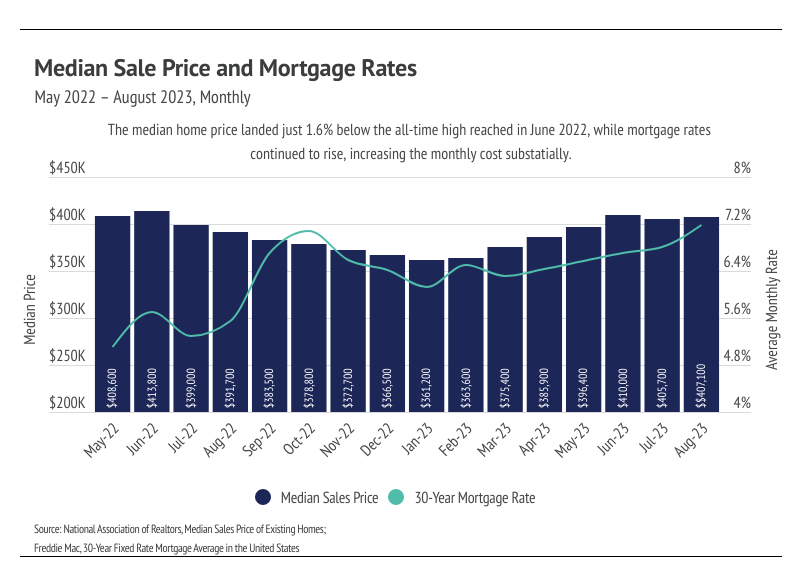

- The national median home price is only 1.6% below the all-time high reached in June 2022, which shows how consistent prices are despite the current interest rates. Home affordability has dropped to its lowest level since the early 1980s when mortgage rates rose above 18%.

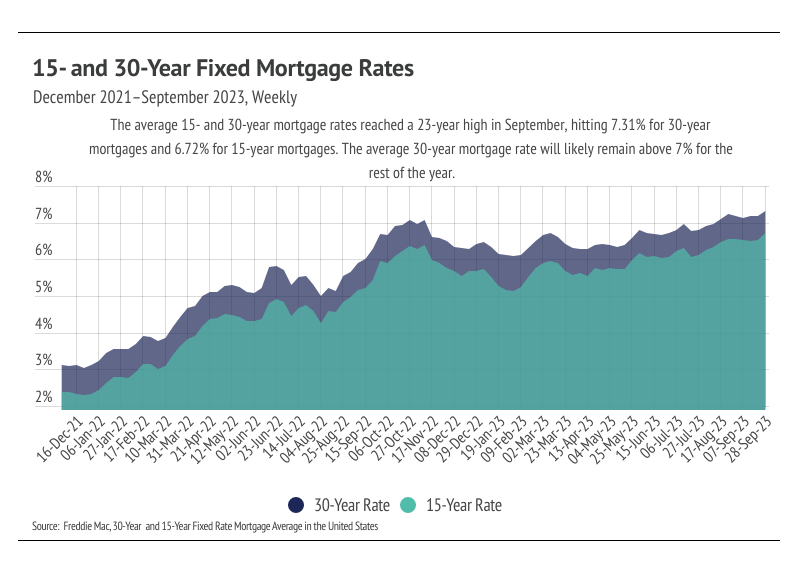

- In September, the average 30-year mortgage rate reached its highest level since December 2020 at 7.31%. Higher interest rates have decreased affordability, pricing many buyers out of the market, and dampened homebuilding, as construction loans have become too costly for builders.

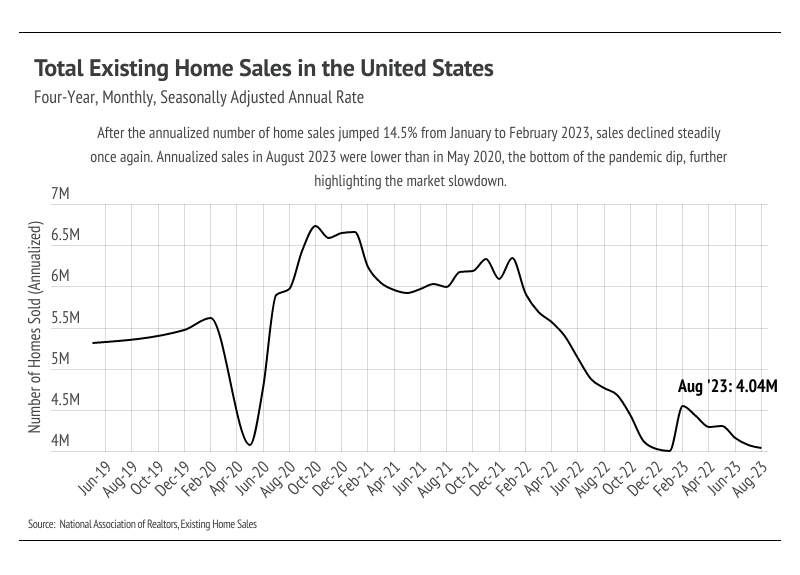

- Home sales have fallen below the initial pandemic dip of May 2020, which further highlights the market slowdown and suggests that the market will remain depressed for at least another six months to a year.

Note: You can find the charts & graphs for the Big Story at the end of the following section.

The great affordability drop

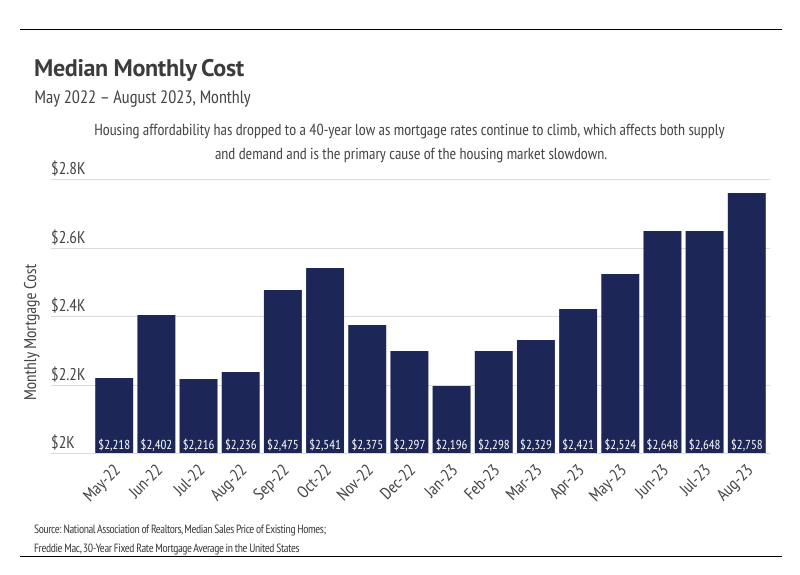

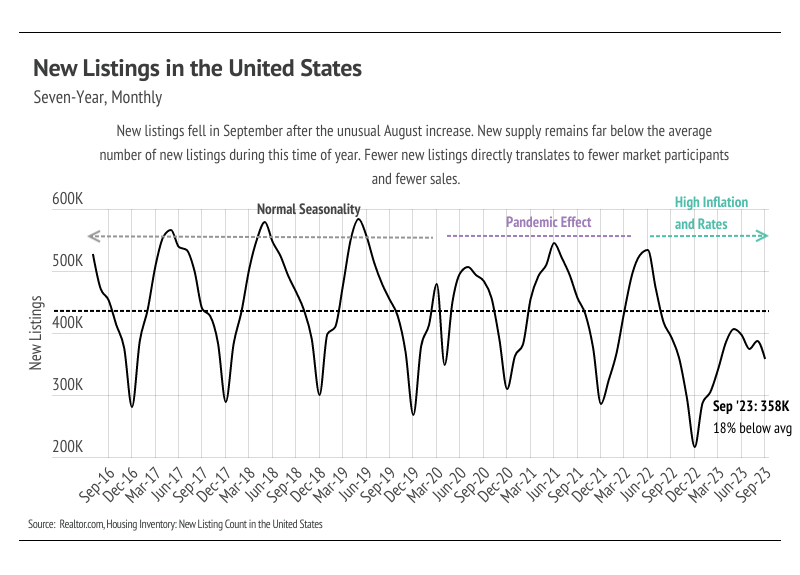

The average 30-year mortgage rate hit a 23-year high in September, closing the month at 7.31%. The current high mortgage rates are negatively affecting affordability, making it incredibly hard not to compare mortgage rates and prices to those of the past few years — because the comparison is so stark. In 2020 and 2021, 30-year mortgage rates were the lowest in history at an average of 3.11% and 2.96%, respectively. Low rates priced buyers into the market, which drastically grew demand in a market with fairly static short-term supply. Competition among buyers rose sharply, increasing prices at the fastest rate ever. The Case-Shiller 20-City Composite Home Price Index rose 41% from June 2020 to June 2022. Meanwhile, inventory plummeted, creating an even larger supply issue than the already undersupplied U.S. market. Although home prices contracted in the second half of 2022, as the Fed began hiking rates, they bounced back in the first half of 2023 and are now only 1.6% below the all-time high. Once we couple the median price with the average 30-year mortgage rate, we can see the actual monthly cost rather than just the price. Only 27% of homes were purchased with cash in August, a good portion of which were likely bought by homeowners selling their home and using the proceeds to buy another. Most buyers, however, are financing the purchase of their homes in some capacity and are, therefore, affected by the high mortgage rates. To put the change into perspective, the median home financed in August 2023 cost 15% more on a monthly basis than the median home financed in June 2022 — the all-time high price — because rates are 1.8% higher.

As you’ve likely already noticed, our current market involves an interesting dynamic of low supply and demand, but high prices and cost of financing. A lot of this has to do with (potential) seller mentality. Approximately 75% of U.S. homeowners have mortgage rates of less than 4%, according to JPMorgan, which has kept potential sellers from entering the market because they either stay in their home or keep their home as a rental property when they move. As a result, new listings remain significantly depressed. When we compare the first three quarters of 2022 and 2023 with the average from the first three quarters of 2017 to 2021, new listings are below average by about 1.5 million homes. The National Association of Realtors reported that the number of homes sold dropped 0.74% month over month and 15.3% year over year, which is less surprising considering that there are far fewer homes from which to choose. That being said, people move for all sorts of reasons, and supply has declined further than demand, which has helped prices stay high. Homebuilders are also affected by higher rates when it comes to construction loans, so homebuilder sentiment is in decline, according to the National Association of Home Builders/Wells Fargo Housing Market Index. We will likely see fewer and fewer new homes built until rates come down, negatively affecting supply.

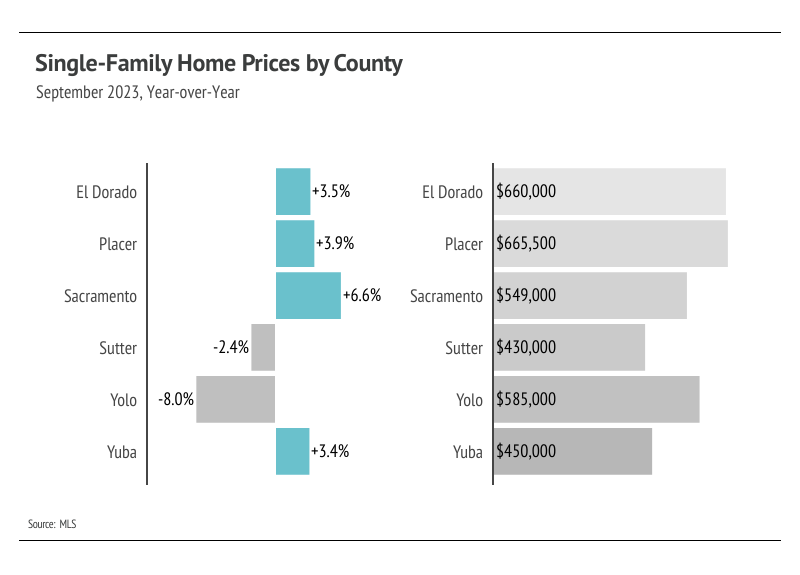

Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage for your area. In general, higher-priced regions (the West and Northeast) have been hit harder by mortgage rate hikes than less expensive markets (the South and Midwest) because of the absolute dollar cost of the rate hikes and limited ability to build new homes. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

Quick Take:

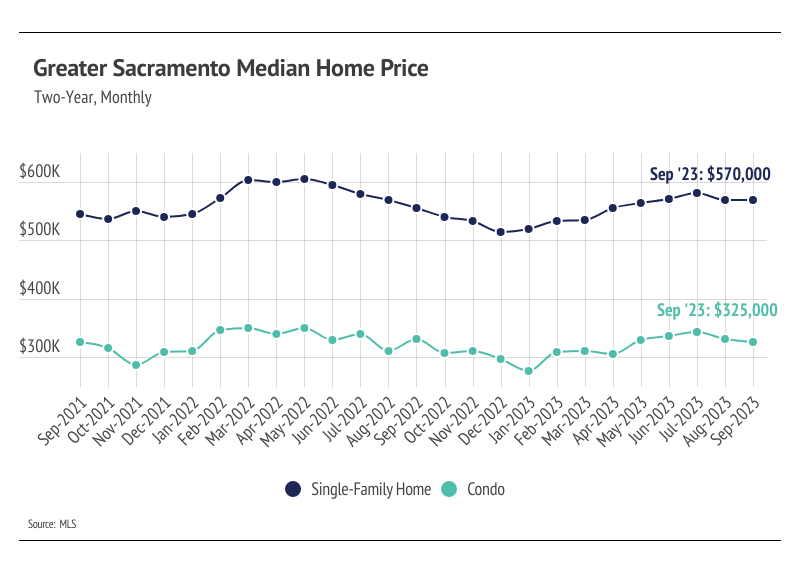

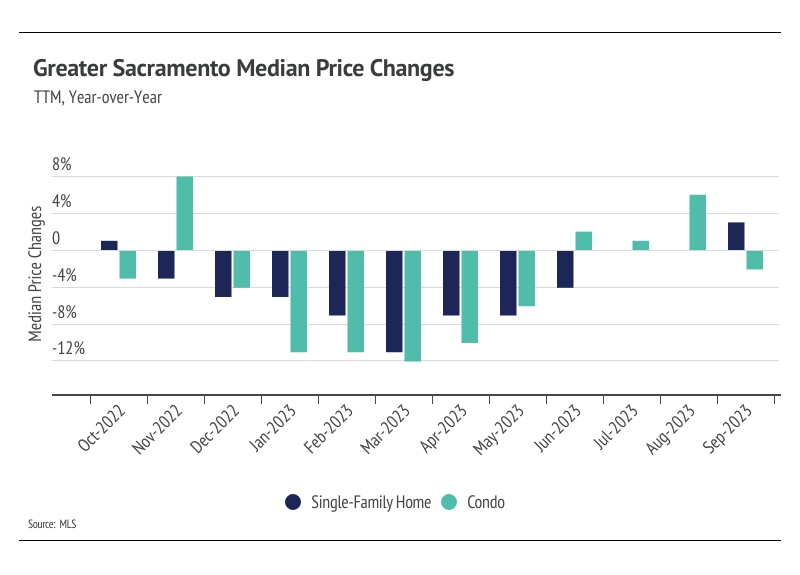

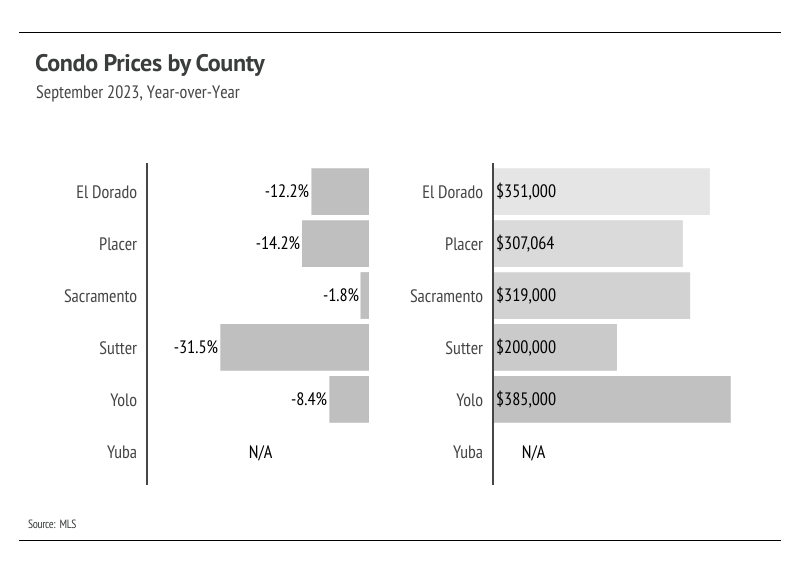

- The median single-family home price rose slightly, while condo prices declined in September. Single-family home prices are only 6% below the all-time high, and we expect prices to remain fairly stable in the fourth quarter.

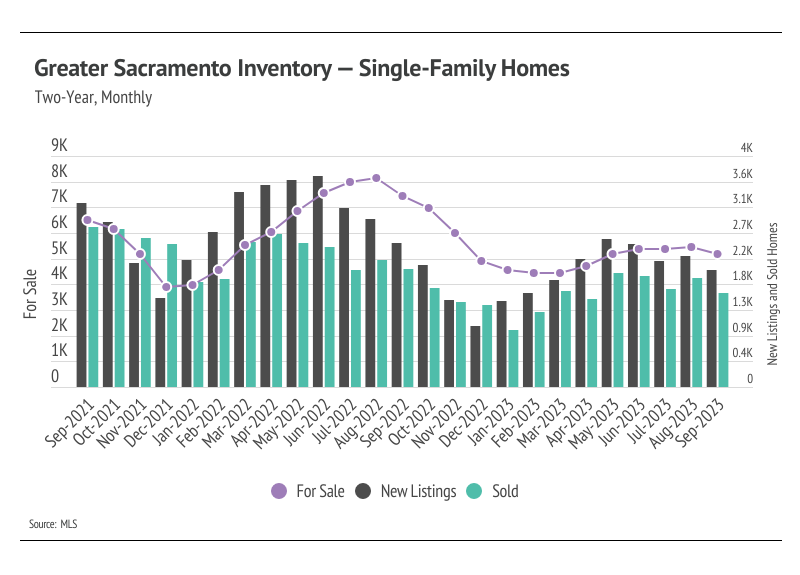

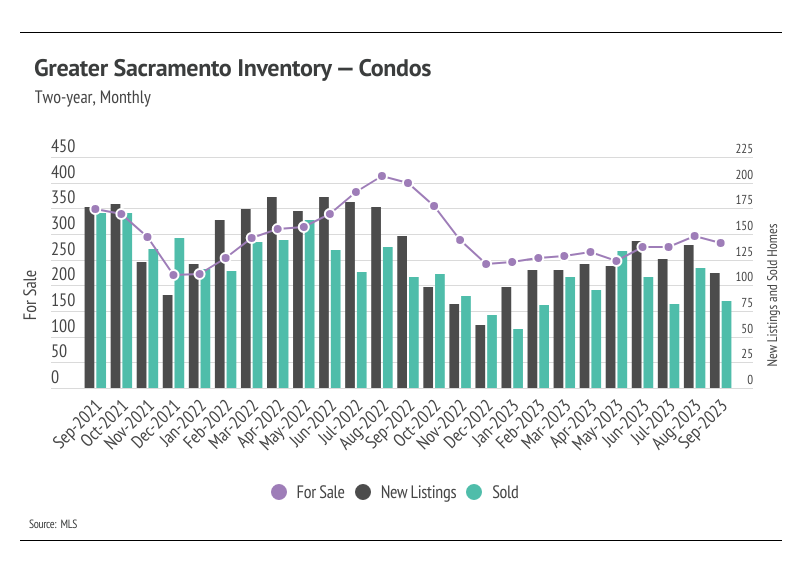

- Active listings in Greater Sacramento fell from August to September, continuing the year-long trend of stagnant inventory levels. Year over year, inventory is still down 27%, highlighting one of the challenges of buying a home in a desirable market.

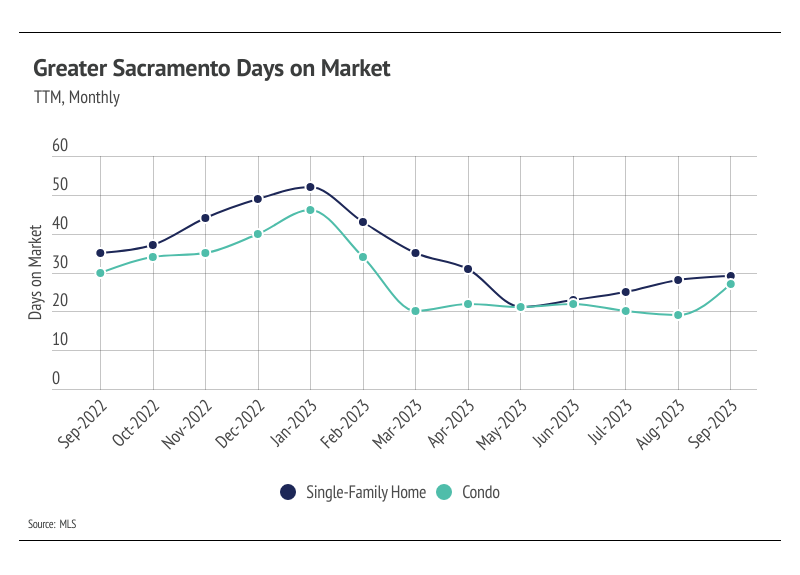

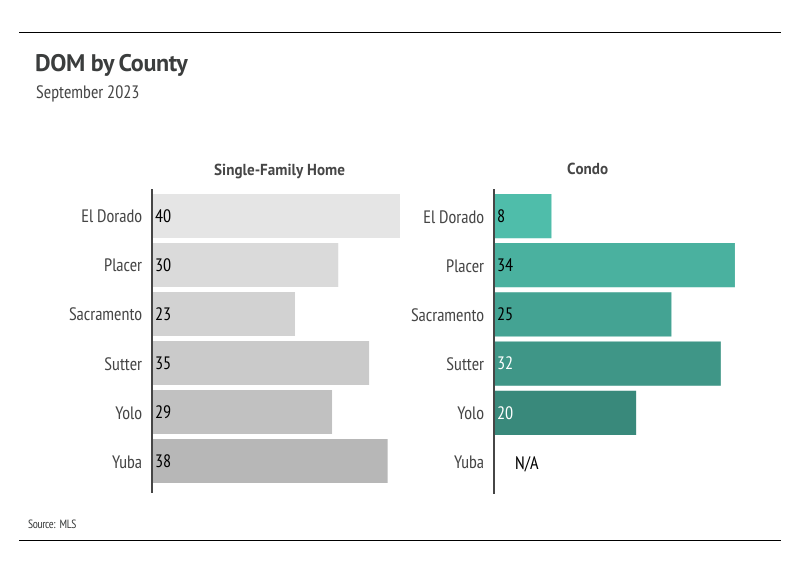

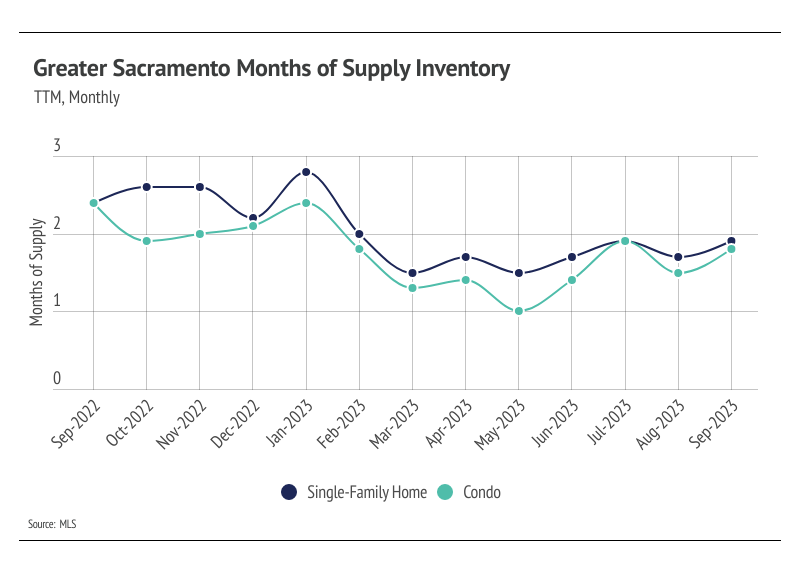

- Months of Supply Inventory rose in September as sales slowed and days on market increased slightly. It’s common for the market to trend toward balance in the fall and winter, when fewer buyers are in the market. Currently, the market still favors sellers.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

Prices fell slightly but remain near record highs

In Greater Sacramento, the price of housing has remained sticky during a period of rapidly rising mortgage rates. Homes are still in the realm of affordable, at least for California, which leads to more market participants.The median single-family home price rose 3% year over year, while condo prices fell 2%. The median single-family home price likely hit the 2023 peak in July, which is inline with normal seasonality. The declining number of new listings will create price support in the slower fall and winter seasons. We expect prices to remain fairly stable in the fourth quarter.

Typically, demand begins to decline in the fall and bottoms out in January, so the consistently low supply should be less of an issue. With mortgage rates at a 23-year high, quality listings are going to have the most competition. This isn’t unusual, but potential homebuyers aren’t nearly as willing to pay a premium for a fixer upper as they were in 2020 and 2021.

Inventory, sales, and new listings declined in September

Since the start of 2023, single-family home inventory has followed fairly typical seasonal trends, but at a significantly depressed level. Low inventory and fewer new listings have slowed the market considerably. This year, sales and new listings peaked in May, while inventory peaked in August. The number of home sales is, in part, a function of the number of active listings and new listings coming to market. Even though demand is softening due to higher interest rates and normal seasonality, inventory is so low that any amount of new listings is good for the market. Comparing new listings from January through September 2023 to the same time period in 2022, new listings are down 32%, which has directly impacted both inventory and sales. Sales are down 20% year over year.

As demand slows, buyers are gaining slightly more negotiating power and paying less than asking price on average. The average seller received 94% of list in January, which grew to 99% by May. The amount sellers are receiving is starting to decline, and by September 2023, the average seller received 97% of list. That being said, inventory will almost certainly remain historically low for the rest of the year, and likely remain low in 2024, which will create price support and at least minor competition among buyers.

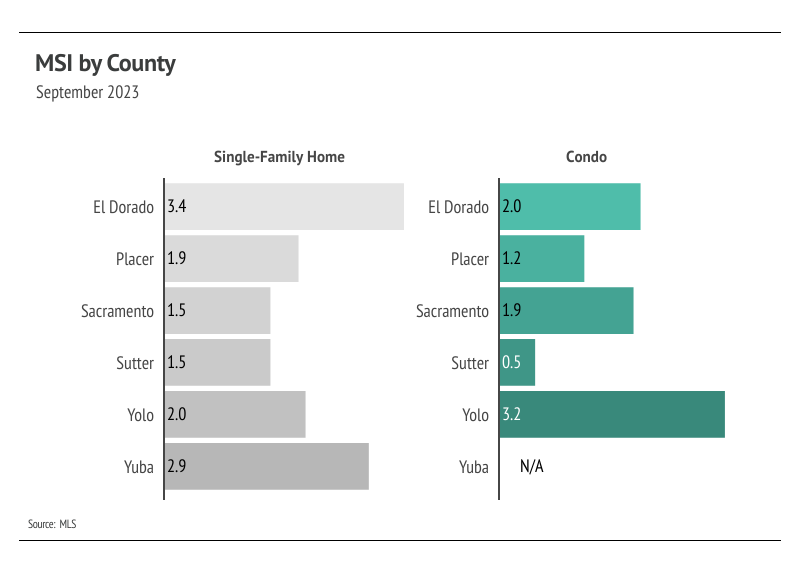

Months of Supply Inventory rose slightly in September but remained under two months of supply, indicating a strong sellers’ market

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI fell sharply in the first quarter this year before gently trending higher in the second and third quarters. MSI remained below two months of supply for both single-family homes and condos, indicating the market still firmly favors sellers.

Stay up to date on the latest real estate trends.

San Diego Market

How to Maximize ROI in La Jolla, North Park & Eastlake

Central Valley Market

What Modesto, Fresno & Stockton Sellers Need to Know About ROI

East Bay Market

Smart ROI Moves for Sellers in Oakland, Berkeley & Walnut Creek

San Diego Market

La Jolla to Chula Vista: It’s Not Always About the Highest Price

Central Valley Market

Stockton to Modesto: What to Consider Beyond the Price Tag

East Bay Market

Beyond Price—What Oakland and Walnut Creek Sellers Should Really Consider

San Diego Market

Why Pre-Listing Inspections Are Gaining Popularity in La Jolla, North Park & Chula Vista

Central Valley Market

Why More Sellers in Modesto, Stockton & Fresno Are Getting Pre-Inspections

East Bay Market

Why Sellers in Oakland, Berkeley & Walnut Creek Are Getting Ahead of Repairs

Allow All City Homes to manage every aspect of your home buying and selling experiences. Our agents ensure transparency, empowerment, and assurance throughout the entirety of your real estate journey, supporting you at each stage.